Little-known benefits of sales ledger financing

- October 30, 2022

According to a 2019 Quickbooks survey, 61% of businesses struggle with cashflow. As a result, 32% of companies can’t pay themselves, loans, suppliers, and employees.

Positive cash flow is the lifeblood of any business. You can’t operate your daily operations on a negative bank balance.

While there are many ways to cushion your business from getting financial blows, not all options are sustainable for every brand.

For example, you can’t depend on running your business on credit. Credit lines might work for huge companies that have already nurtured good relationships with financial institutions.

On the other hand, small businesses or startups face a challenging qualification process, which frequently prevents them from accessing funds.

Either way, sales ledger financing works well for any type of business. Stay tuned as we delve all into sales ledger financing to see how you can use it to avoid insufficient cashflow.

What is Sales Ledger Financing?

Cashflow problems arise when customers begin to pay invoices late. Ideally, customers take around 14-30 days to pay invoices, depending on your payment terms.

However, research has it that most customers pay invoices six days late. 20% go past two weeks, 33% go past a month, and another 20% take at least 60 days. The worst part? You’ll still incur more costs if you decide to follow up on unpaid invoices.

Regardless of your business size, cashflow problems are inevitable if these are your customers.

Enter sales ledger financing (interchangeably used with “invoice discounting”).

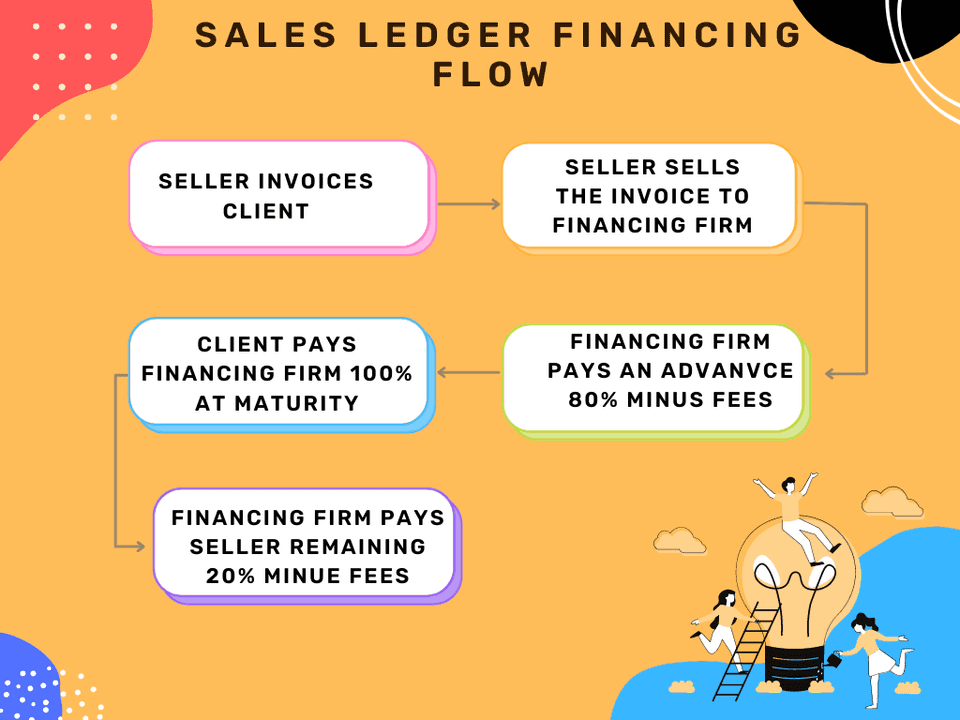

Sales ledger financing is a simple way to get your invoices paid sooner. But you won’t have to hold a gun on your customer's head to get your money.

It’s simply handing over your account receivables to a lender in exchange for an immediate cash injection to your business.

The sales ledger finance financing firm gives you a large percentage (around 80-90%) of the amount and will reimburse the remainder once your client pays after taking a small fee cut.

For example, a B2B company selling logistic services to brands might have some clients paying 30, 40 or even 60 days after sending the invoice.

So instead of waiting that long, you sell the invoice you billed to your customers to a third party company - a sales ledger financing institution.

The financing institution will then pay a certain percentage of the face value of the invoice (let’s say 80%).

A couple of days later, when your customer pays the invoice, the financing institution will give you the last 20% but take a small cut as a service fee.

Multiple sales ledger financing institutions charge differently for their service. The cost is mainly affected by the invoice value, the creditworthiness of your client, the length of the commercial relationship, and the days financed.

Let’s look at how much it will cost to get funded by a sales ledger financing institution with a 2% fee for 60 days.

| Invoice value | Days financed | Advance payment | % fee | Balance received at invoice maturity |

|---|---|---|---|---|

| $10,000 | 60 | $8,000 | 2% | $8,800 |

| $30,000 | 60 | $24,000 | 2% | $5,400 |

| $50,000 | 60 | $40,000 | 2% | $9,000 |

| $100,000 | 60 | $80,000 | 2% | $18,000 |

That said, most people often confuse between invoice discounting (sales ledger finance) and invoice factoring. That’s what we’ll discuss in the next section.

Difference between Invoice Factoring and Sales Ledger Finance

Both forms of business financing have a common goal - to improve your business cash flow so that you can efficiently manage your daily operations. Plus, they help by financing your open invoice from slow-paying but credit-worthy customers.

The only difference is that a factoring company takes control of your sales ledger and does the debt collection from you.

On the other hand, a sales ledger financing company only does the prepayment and waits for you to do all the other credit control tasks.

That said, here are four key differences between the two.

-

Size of companies: Invoice factoring is designed for small businesses with a short track record that needs quick cash injections. Sales ledger invoicing suits big companies that have outgrown invoice factoring and receive a minimum sales revenue of $200,000 per month.

-

Process of Funding: You need a lot of paperwork to get the funds from an invoice factoring firm. For example, you must submit a legal document known as the _schedule of accounts t_hat shows every invoice you want to fund.

Furthermore, you need backup documentation to verify that you offered the service/product you’re seeking payment for.

On the other hand, sales ledger finance only requires a copy of your sales ledger, which your accounting team can quickly generate.

- Invoice verification process: Invoice factoring takes much time to verify invoices and ensure they’re accurate, but it often takes longer, which delays funding.

Sales ledger financing has an equally thorough approach but makes the process simpler.

The process is quite similar to that line of credit, meaning you won’t have to contact your customer hence less friction in your customer relationship.

Below are more differences that separate invoice factoring and sales ledger finance.

| Sales Ledger Finance | Invoice Factoring |

|---|---|

| Does not include full sales ledger and collections service. | Provides value-added services such as full sales ledger and collections service. |

| The customer doesn’t know that you’ve sold the invoice to a sales ledger invoice firm. | The customer knows that the invoices have been factored in. |

| In sales ledger financing, your business collects the invoices and deals with the book debt collections process; hence cheaper. | Factoring is more expensive than invoice discounting because you are paying for an outsourced collections department with a factoring facility. |

Advantages of Sales Ledger Financing

Better customer experience

Sales ledger financing is easier to use than invoice factoring. You only need to submit your sales ledger on your side. No need to stress your accounting team to produce invoices and extra documentation before applying for funds.

On the other hand, your customers don’t have to deal with the stress of verifications from a sales ledger financing firm. This is handy when dealing with sensitive clients, as it strengthens relationships.

Easier to get than bank loans and credits

Lines of credit work well if you can meet all the requirements and have a solid financial statement with many assets to work as collateral.

Unfortunately, only a few fortune companies can possess all of this simultaneously. Sales ledger financing is an escape route for businesses that cannot afford all this at once.

You’re good to go as long as your company has a track record of profitability, your financial statement is in good standing, and you deal with credit-worthy customers..

Quick Application Process

Getting funds from a sales ledger financing firm is a relatively straightforward process. It doesn’t have the numerous steps you’ll experience in a line of credit or invoice factoring.

The first thing to do is to submit an application form for funding. You should add updated financial statements like profit and loss statements, balance sheets, accounts payable aging, and your sales ledger.

Better rates

Sales ledger rates are far much better when compared to invoice factoring and credit lines because it’s offered to companies that have outgrown the restrictions of an invoice factoring firm.

Furthermore, the rates are applied on monthly average use. That means it falls somewhere between invoice factoring charges and credit line costs.

A step-up to a line of credit

You can use a sales ledger financing program to get more affordable funding methods like bank loans.

When used strategically and you don’t have issues with missed payments, you can upgrade to borrowing from a base certificate program like asset-based loans or even full-suit lines of credit.

Disadvantages of Sales Ledger Finance

Sales ledger financing is undoubtedly a reliable way to get funds. But still has a few critical flaws.

Short repayment periods

Sales ledger financing has short repayment terms because you pay back when your customer fulfills the invoice. This means you have shorter repayment terms hence higher APRs.

Undetermined fees

Sales ledger financing costs relies on the duration it takes before your customers pay the invoice. This means you don’t have total control over how exactly your sales ledger financing is costing you.

Bottom line

Sales ledger financing is a surefire option to get funding when you need to boost your cash flow. It’s not only reliable but also more flexible than other financing sources than factoring and credit lines.

Written by

Jeppe Liisberg

Jeppe Liisberg is a forward-thinking entrepreneur and software developer who has built and contributed to multiple successful startups. With a philosophy centered on creating focused, specialized solutions that excel at solving specific challenges, Jeppe founded Myphoner after identifying a critical gap in the market for effective cold calling software.

"I believe that exceptional software should solve one core problem extraordinarily well rather than attempting to be everything for everyone," says Jeppe. "After years in the trenches as an entrepreneur, I couldn't find a cold calling solution that truly met the needs of small businesses and sales teams—so I built Myphoner to fill that void."

Today, Jeppe remains personally invested in Myphoner's success and customer satisfaction, personally welcoming new users and actively responding to feedback. This hands-on approach ensures that Myphoner continues to evolve based on real user needs while maintaining its commitment to simplicity, effectiveness, and affordability.

Connect with Jeppe on LinkedIn or reach out directly at jeppe@myphoner.com.

Related articles

Tools & Practises

The Complete 2023 Call Queues Guide and Tips for Improving Your Call Queues

Call queues manage incoming calls in businesses. Learn how to set up efficient queues with prioritization, time-based routing & custom greetings. Boost your CX!

April 27, 2023

Tools & Practices

Achieving Significant Results with Strategic Phone Follow-ups on LinkedIn

Learn how to boost LinkedIn campaign conversions to 40% or more: warm call follow-ups raised appointment bookings from 15% to 40% in a diverse industry case study

March 29, 2023

Tools & Practices

LeadFuze Review - Transforming the way you generate leads

Boost sales with effective lead generation using LeadFuze. Our guide explores what it is and how to use it effectively to identify potential customers with ease.

March 9, 2023